Investment Analysis: Kabra Extrusion

Right place at the right time; but now the times have changed

Kabra Extrusion has given shareholders a 5x return in the last 3 years. A stellar performance. This was on the backs of their new business vertical: Battery pack production for EV 2 wheelers.

The traditional business isn’t one of high growth (~8%) so it will never justify the lofty PE (40) that the stock is currently enjoying. So underwriting has to happen for the battery business.

So what is the battery pack business?

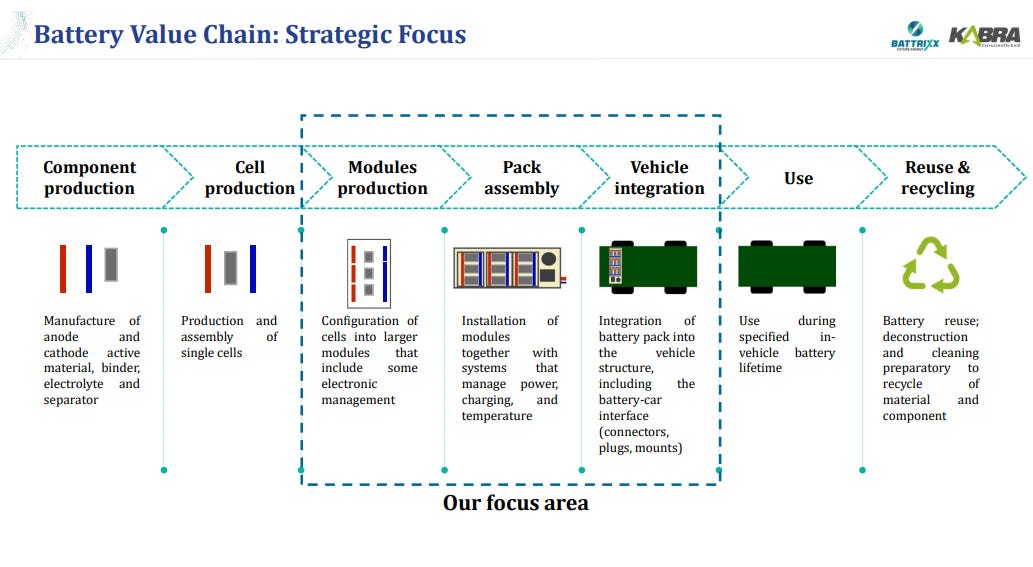

EVs need batteries to operate and this involves taking components of the cell (anode, cathode etc) and making them into a cell it self, which is then made into modules (collection of cells) which is then integrated useing a BMS (Battery management system) into a Battery Pack and installed into the vehicle (see image below). Kabra Extrusion isn’t working across the value chain but only from Module Production to Vehicle Integration.

Why don’t the EV manufacturers do this themselves?

Its seems like the larger players all plan to just that. Its the smaller players like Ampere, who might not have the capital or bandwidth to setup battery pack unit that might continue to need players like Kabra Extrusion.

What I understand the battery packs production is not a highly specilized role as of now and no major differentiation exists. Furthermore, pricing power is poor (even if input prices rise) as consumer will simply stop buying EV and switch to ICE vehicle if the prices rise too much.

There is some talk of building deep insights by collecting performance data in the Kabra Extrusion presentations but this seems more of ambition than reality as of now.

If all this is true, then how are they growing so fast?

They were simply at the right place at the right time. In June 2021, GOI announced an incentive of 2 wheeler EVs which saw a sharp rise in their adoption. But then the incentive was removed from June 2023 and you can see a sharp drop in the growth rate of EV 2 wheeler sales (image below).

Kabra’s battery division revenue has followed a similar trajectory.

So what is the bottom line?

Kabra Extrusion is another momentum play in my opinion and now the momentum is over. There is no reason to believe as of that the traditional business (Extrusions) will suddenly show explosive growth and even if the battery business grows along with industry, the weighted growth will only be 13% of topline. With fluctuating raw material prices and lack of pricing power, the EPS might not grow consistently at 13%. But even if it does, 13% EPS growth does not deserve a 40 PE for a company of the size of Kabra Extrusion and in an industry that is far from being stable as of now.

Nice Analysis, They have put up capacity, they are foraying into E3 and E4 , Gov may consider some form of incentive to pursue EV adoption in future. Do you think the current performance is the bottom and business could look up from 2 qtr down the line?